What Should An HOA Budget Template Have?

Every homeowners association relies on a carefully crafted budget for its yearly expenses. But, what does an HOA budget template look like? And what should it include?

What Is an HOA Budget Template? Why Is It Important?

Homeowners associations operate on an annual budget usually prepared by the HOA board or the budget committee. This budget serves as a guide that the board will use for the coming year’s expenses. Additionally, it is from this budget that homeowner dues are calculated.

It’s easy to say that an HOA budget is important. But, what exactly makes it so essential to a homeowners association?

First of all, the HOA budget has a direct impact on the association’s finances. Any board that uses a “go with the flow” approach to its expenses is destined to drive its HOA into financial ruin. The budget acts as your board’s guide — letting you know what you should spend money on and how much. This ensures that you don’t spend too much on a single line item and run out of money for other necessary expenses.

Secondly, the HOA budget allows you to determine how much to charge owners in dues. Without a template, you may end up charging too little or too much, which are both equally bad. Charging too little will put your association in a deficit and force you to levy special assessments. On the other hand, charging too much could tempt you into spending more money than necessary, simply because the funds are available.

A budget template also makes it easy for the board to plug in amounts for the expenses. This allows for a smoother and stress-free budget planning session for everyone involved.

Finally, the HOA budget template allows for transparency in your association. Homeowners have a right to know where their money is going, and the budget addresses that. In some states, the board is even required to present the budget to the membership for ratification. North Carolina, for instance, has such requirements for both HOAs and condominiums.

What Is Included in an HOA Budget Template?

You already know that the HOA budget plays a critical role in an association’s finances. Of course, there is a difference between saying you need a budget and actually preparing the budget. What should an HOA budget template even include anyway?

Expected Income

The first part of any HOA budget should cover the expected income or earnings of the association. This usually comes in the form of dues and assessments, though it can also include things like interest income.

If your association rents out its common facilities or amenities, income earned from rentals will fall under this section as well. Of course, it is not always possible to anticipate rental income for the coming year, unless it is a fixed event that happens annually.

Anticipated Expenses

The expenses portion of the HOA budget template is typically divided further into sections. There is no single correct way to prepare this part of the budget, as different HOAs may adopt varying styles. However, it is important to create an organized format that homeowners can easily interpret.

The following sections typically appear under the “expenses” portion of the HOA budget:

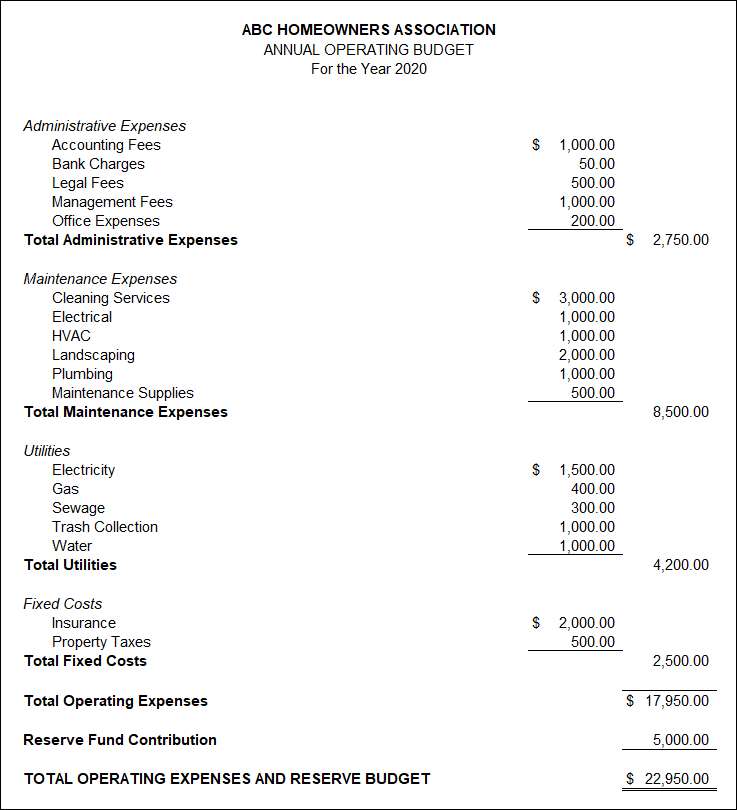

- Administrative Expenses. This includes management fees, legal fees, bank charges, office supplies, the cost of preparing newsletters, and even reserve studies.

- Maintenance Expenses. Line items under this section can include landscaping costs, cleaning services, maintenance supplies, electrical costs, plumbing costs, and the like.

- Utilities. Under utilities, you have expenses such as gas, water, electricity, sewage, phone bills, and even trash collection costs.

- Fixed Costs. This includes recurring costs that usually come at a fixed rate such as insurance premiums, property taxes, and annual report filing fees (Secretary of State).

Reserve Contributions

Lastly, every HOA budget should include reserve contributions. This is the amount the association should set aside in its reserve fund for future major repairs or replacements. The board must maintain the proper reserve level, which is usually 70 percent funding. To know how much is considered fully funded for your HOA, it is important to conduct a reserve study.

Sample HOA Budget

Make your budget planning season easier and less stressful with the help of the homeowners or condo association budget template below.

Download Your HOA Budget Excel Template Here

Tips for Planning Your Next HOA Budget

Preparing an annual budget for your association can come as a challenge, especially if you don’t have a background in budgeting or have simply never done it before. As part of your HOA board, though, it is one of your duties to plan for the coming year’s expenses. Here are some tips you can use when drafting your next HOA budget.

1. Review Past Budgets and Reports

One of the best ways to ensure you’re on the right track is to look at past budgets and financial reports. When you do this, you can determine how much you spent on every line item in the previous years. This will give you an idea of how much you should expect to spend this year. Reviewing past reports is always a good place to start when you are planning your HOA budget.

2. Send Out RFPs

While it is good practice to review past budgets, they can only tell you what happened in previous years. But, things can change over time.

While it is good practice to review past budgets, they can only tell you what happened in previous years. But, things can change over time.

For instance, vendors can increase their rates or give special discounts. Before preparing your budget, it is a good idea to send out requests for proposals to vendors and suppliers. Doing this will allow you to gauge how much to allocate per service or expense.

3. Add a Buffer

This may seem like an obvious tip, but it still needs to be said. When planning your HOA budget template, don’t forget to add a buffer. Doing so will give you extra room in the budget to cushion unexpected costs or unforeseen increases. Of course, it is equally important not to go overboard with your buffer.

Easy HOA Budget Planning

The homeowners association budget preparation season can be a taxing period for HOA board members, but it doesn’t have to be that way. With an HOA budget template, you can easily input the expenses and amounts you expect for the year. From there, you can determine how much each homeowner has to pay in dues.

Of course, with Condo Manager’s HOA management software, budget planning is made even simpler. With a dedicated budget planning module, all you need to do is plug in the numbers and let the software do the rest. You can even export the budget as you see fit. Call us today at (800) 626-1267 or contact us online to set up a free demo.

RELATED ARTICLES:

- What Are HOA Reserve Funds? And What Is It For?

- HOA Accounts Payable Report: What Is This For?

- HOA Account Delinquency Report: Does Your HOA Need One?

Dues and assessments are the lifeblood of every homeowners association. Without them, an HOA community would suffer detrimental consequences.

Dues and assessments are the lifeblood of every homeowners association. Without them, an HOA community would suffer detrimental consequences. While it is required for some associations to share the total delinquency amount to homeowners, a majority are not allowed to disclose detailed information. In Nevada, for instance, the law

While it is required for some associations to share the total delinquency amount to homeowners, a majority are not allowed to disclose detailed information. In Nevada, for instance, the law

Unfortunately, not all HOA board members have a background in accounting. This makes it difficult to prepare financial reports, including the accounts payable report. While many turn to HOA management companies or accountants for help, another alternative is to invest in software.

Unfortunately, not all HOA board members have a background in accounting. This makes it difficult to prepare financial reports, including the accounts payable report. While many turn to HOA management companies or accountants for help, another alternative is to invest in software.

The general ledger acts as the master copy of all financial transactions in a homeowners association. It contains all accounting data, including those posted from your sub-ledgers and journals. Therefore, an HOA general ledger should include all

The general ledger acts as the master copy of all financial transactions in a homeowners association. It contains all accounting data, including those posted from your sub-ledgers and journals. Therefore, an HOA general ledger should include all  Accrual accounting is the most widely used approach because of its accuracy and reliability. It is also the only accounting method that conforms with the

Accrual accounting is the most widely used approach because of its accuracy and reliability. It is also the only accounting method that conforms with the

Operating Activities. This part consists of cash sourced from and spent on business activities. For an HOA, that could mean

Operating Activities. This part consists of cash sourced from and spent on business activities. For an HOA, that could mean  On paper, the homeowners cash flow statement seems easy to prepare. But, it actually takes a lot of organizing, cross-checking, and discipline to properly put one together. Many companies have teams of accountants and professionals for this kind of task. Homeowners associations, though, typically only have their board to rely on.

On paper, the homeowners cash flow statement seems easy to prepare. But, it actually takes a lot of organizing, cross-checking, and discipline to properly put one together. Many companies have teams of accountants and professionals for this kind of task. Homeowners associations, though, typically only have their board to rely on.

Homeowners associations function in much the same ways as a business. And just like a business, HOAs need financial statements to guide their financial decisions.

Homeowners associations function in much the same ways as a business. And just like a business, HOAs need financial statements to guide their financial decisions. While many associations hire an accountant or a management company to help prepare their financial reports, you can achieve equally great results with management software.

While many associations hire an accountant or a management company to help prepare their financial reports, you can achieve equally great results with management software.

It is the homeowners association’s job to maintain the common areas of a community. When you have a particularly large community, though, maintenance issues can quickly multiply.

It is the homeowners association’s job to maintain the common areas of a community. When you have a particularly large community, though, maintenance issues can quickly multiply. It is nearly impossible to keep up with the demands of multiple communities at once when using manual processes.

It is nearly impossible to keep up with the demands of multiple communities at once when using manual processes.

If you ask anyone on an HOA board what the most challenging aspect of running an HOA is, chances are most people will say financial management.

If you ask anyone on an HOA board what the most challenging aspect of running an HOA is, chances are most people will say financial management. Whether your software is cloud-based or relies on a local server, you can’t deny that having easy access to data is a huge benefit. When you do things manually, you tend to organize your paperwork into piles or drawers. Searching for documents requires time and a lot of flipping through pages. Software, though, makes this process infinitely simpler. You can search for documents using keywords and organize them with just a few clicks.

Whether your software is cloud-based or relies on a local server, you can’t deny that having easy access to data is a huge benefit. When you do things manually, you tend to organize your paperwork into piles or drawers. Searching for documents requires time and a lot of flipping through pages. Software, though, makes this process infinitely simpler. You can search for documents using keywords and organize them with just a few clicks.

Even though an HOA management software is a useful tool, and not just during times of crisis, many homeowners associations still feel hesitant about purchasing one.

Even though an HOA management software is a useful tool, and not just during times of crisis, many homeowners associations still feel hesitant about purchasing one. Given the highly contagious nature of COVID-19, homeowners associations should avoid holding in-person meetings. This includes board meetings and annual or general assembly meetings, especially in enclosed or indoor spaces.

Given the highly contagious nature of COVID-19, homeowners associations should avoid holding in-person meetings. This includes board meetings and annual or general assembly meetings, especially in enclosed or indoor spaces.